RETIREMENT PLANNING &

INCOME STRATEGIES

Retirement Planning & Income Strategies

Secure Your Future. Enjoy Your Retirement.

Retirement planning is about more than just saving; it’s about creating a comprehensive strategy to ensure you can live the retirement you’ve always dreamed of, without worrying about outliving your resources. It’s about making informed decisions now to secure your financial freedom later.

At Pinnacle Financial Solutions, we help Canadians develop personalized retirement plans that address their unique needs, goals, and risk tolerance. We specialize in helping IT professionals, business owners, and high-net-worth individuals navigate the complexities of retirement planning.

Why Start Planning Now?

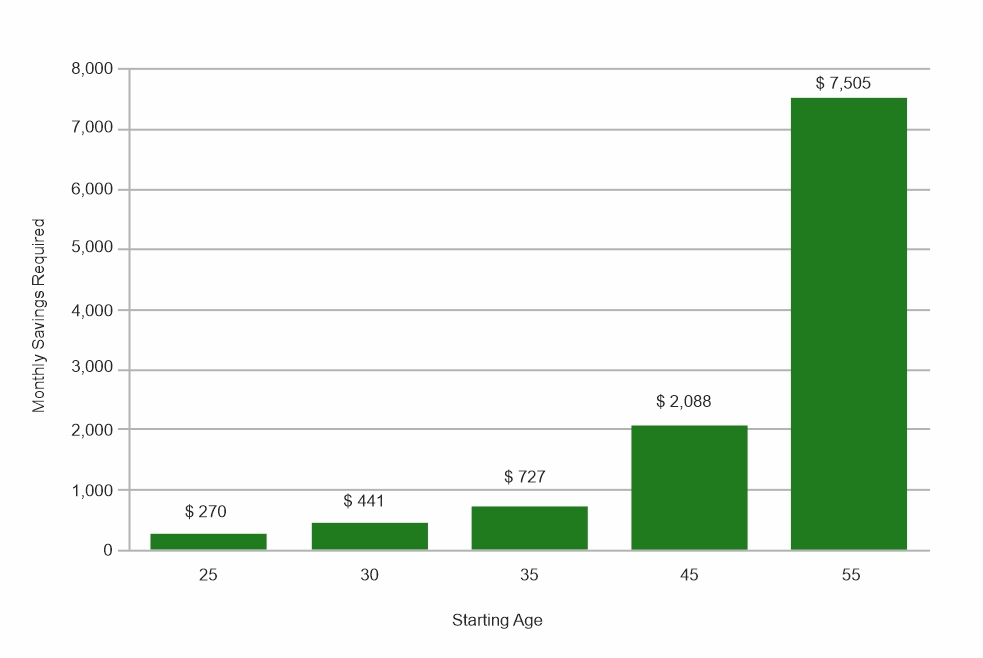

The sooner you start planning for retirement, the better. The power of compound interest means that even small, consistent contributions made early in your career can grow significantly over time. Delaying retirement planning can dramatically increase the amount you need to save each year to reach your goals. Most Canadians would need 1.5M to have a comfortable retirement and to reach this number you’d need to save the following

The Impact of Starting Age:

* This table is a general illustration and assumes consistent saving and a 10% annual return.

Actual investment returns may vary. This is not a guarantee of future performance.

As you can see, starting early makes a huge difference!!

Now The Key Questions to Ask Yourself:

- What’s your ideal retirement? Travel? Hobbies? Volunteering? Spending time with family?

- When do you want to retire? Early? At 65? Later?

- How much income will you need? Aim for 70-80% of your pre-retirement income as a starting point, but personalize it. Many Canadians require around 1.5M to have a comfortable retirement.

- What are your income sources? CPP, OAS, workplace pensions, personal savings, investments?

- How will you manage healthcare costs?

- How will you protect against inflation?

- How will you minimize taxes in retirement?

Our Personalized Planning Process

We take a holistic and personalized approach to retirement planning. Our process typically includes:

- Discovery: Understanding your goals, values, current financial situation, and vision for retirement.

- Assessment: Analyzing your income, expenses, assets, liabilities, and existing retirement savings.

- Projection: Estimating your future income needs and developing a savings strategy.

- Investment Strategy: Creating a diversified, tax-efficient portfolio aligned with your risk tolerance and time horizon.

- Withdrawal Strategy: Planning how you’ll access your funds in retirement to maximize income and minimize taxes.

- Insurance Planning: Reviewing your insurance coverage (life, disability, long-term care) to mitigate risks.

- Estate Planning: Integrating your retirement plan with your overall estate plan.

- Regular Reviews: Adjusting your plan as needed to reflect changes in your life, goals, and the economic environment.

Understanding Your Retirement Income Sources

Canadians typically rely on a combination of:

- Canada Pension Plan (CPP): A contributory, earnings-related program. You can start as early as 60 (reduced benefit) or as late as 70 (increased benefit).

- Old Age Security (OAS): A monthly benefit for most Canadians 65+. High-income earners may face clawbacks.

- Guaranteed Income Supplement (GIS): For low-income OAS recipients.

- Workplace Pension Plans: Defined Benefit (DB) or Defined Contribution (DC) plans, or Group RRSPs.

- Personal Savings & Investments: RRSPs, TFSAs, non-registered accounts, real estate.

Are You Taking Advantage of Workplace Benefits?

Many Canadians overlook valuable workplace benefits that can significantly boost their retirement savings:

- Registered Pension Plans (RPPs): Often with employer matching – essentially “free money.”

- Group RRSPs: Tax-advantaged savings with potential employer contributions.

- Deferred Profit-Sharing Plans (DPSPs): Benefit from your company’s profits.

Make sure you’re maximizing these opportunities!

Minimizing Taxes in Retirement: Key Strategies

- Strategic Withdrawals: Carefully plan the order in which you withdraw funds from your various accounts (RRSPs/RRIFs, TFSAs, non-registered) to minimize your overall tax burden.

- Pension Income Splitting: If eligible, split pension income with a spouse to reduce your combined tax liability.

- CPP/OAS Timing: Consider the optimal timing for starting your CPP and OAS benefits.